|

|

|

|

Name

Cash Bids

Market Data

News

Ag Commentary

Weather

Resources

|

It's Time Investors Give Qualcomm Stock a Little 'Respect'/Qualcomm%2C%20Inc_%20logo%20on%20phone-by%20viewimage%20via%20Shutterstock.jpg)

Qualcomm (QCOM) stock ticked lower yesterday after the bell despite delivering a solid fiscal third-quarter earnings beat. Despite since bouncing back today, this dip highlights what analysts say is a persistent lack of "respect" for the semiconductor giant that investors should reconsider. The wireless technology leader reported fiscal third-quarter revenue of $10.4 billion, topping analyst estimates of $10.34 billion with a 10% year-over-year increase. Non-GAAP earnings per share of $2.77 exceeded forecasts by 2.2%, yet the market's lukewarm response underscores ongoing skepticism about the company's prospects.

What investors may be missing is Qualcomm's successful pivot beyond smartphones. While handset chip revenue grew a modest 7% to $6.3 billion, the company's diversification strategy is gaining serious traction. Automotive revenue surged 21% to $984 million, hitting a quarterly record, while Internet of Things (IoT) revenue jumped 24% to $1.7 billion. The company's expansion into artificial intelligence (AI) infrastructure and PC processors, with its Snapdragon X platform, is expected to power over 100 PC models by 2026. The recent $2.4 billion acquisition of Alphawave Semi strengthens its data center capabilities as AI demand continues to surge. Qualcomm returned $3.8 billion to shareholders through dividends and buybacks while maintaining healthy margins. In fiscal 2025 (ending in September), Qualcomm is forecast to pay an annual dividend of $3.59 per share, up from $3.51 per share in fiscal 2024. Moreover, these payouts are forecast to increase to $3.91 per share in fiscal 2028. Is Qualcomm Stock a Good Buy Right Now?Qualcomm recently unveiled an ambitious road map to reach $22 billion in combined automotive and IoT revenues by fiscal 2029. Nakul Duggal, GM of Auto, IoT, and Cloud, highlighted Qualcomm's decade-long transformation of automotive architecture through its Snapdragon Digital Chassis platform. Qualcomm’s safety-certified Advanced Driver-Assistance System (ADAS) stack will debut globally with BMW's Neue Klasse vehicles, marking a key milestone in autonomous driving technology. With 20 OEMs programmed for Autopilot solutions launching within 18 months, Qualcomm is positioned to capitalize on the growing demand for ADAS. The automotive segment's $45 billion design win pipeline includes substantial ADAS opportunities, with management noting that one-third of this backlog represents the next major growth driver beyond traditional infotainment systems. CEO Cristiano Amon also revealed advanced discussions with a leading hyperscaler for custom ARM-based solutions, targeting fiscal 2028 revenue generation. The $2.4 billion Alphawave IP acquisition provides critical connectivity IP to complement Qualcomm's Oryon CPU and Hexagon NPU processors. Management emphasized their focus on inference optimization, targeting efficiency metrics like tokens per dollar and tokens per watt as AI workloads scale. Moreover, the multi-year Xiaomi agreement ensures Snapdragon 8 Series platforms will power flagship devices with increasing volumes annually across China and global markets. This partnership will help Qualcomm strengthen its position in China, where the company has operated successfully for three decades. Qualcomm's diversification strategy appears well-positioned for sustained growth across multiple high-value markets. What is the Target Price for QCOM Stock?Analysts tracking QCOM stock expect sales to rise from $39 billion in fiscal 2024 to $47 billion in fiscal 2028. In this period, adjusted earnings are forecast to expand from $10.2 per share to $13.3 per share.

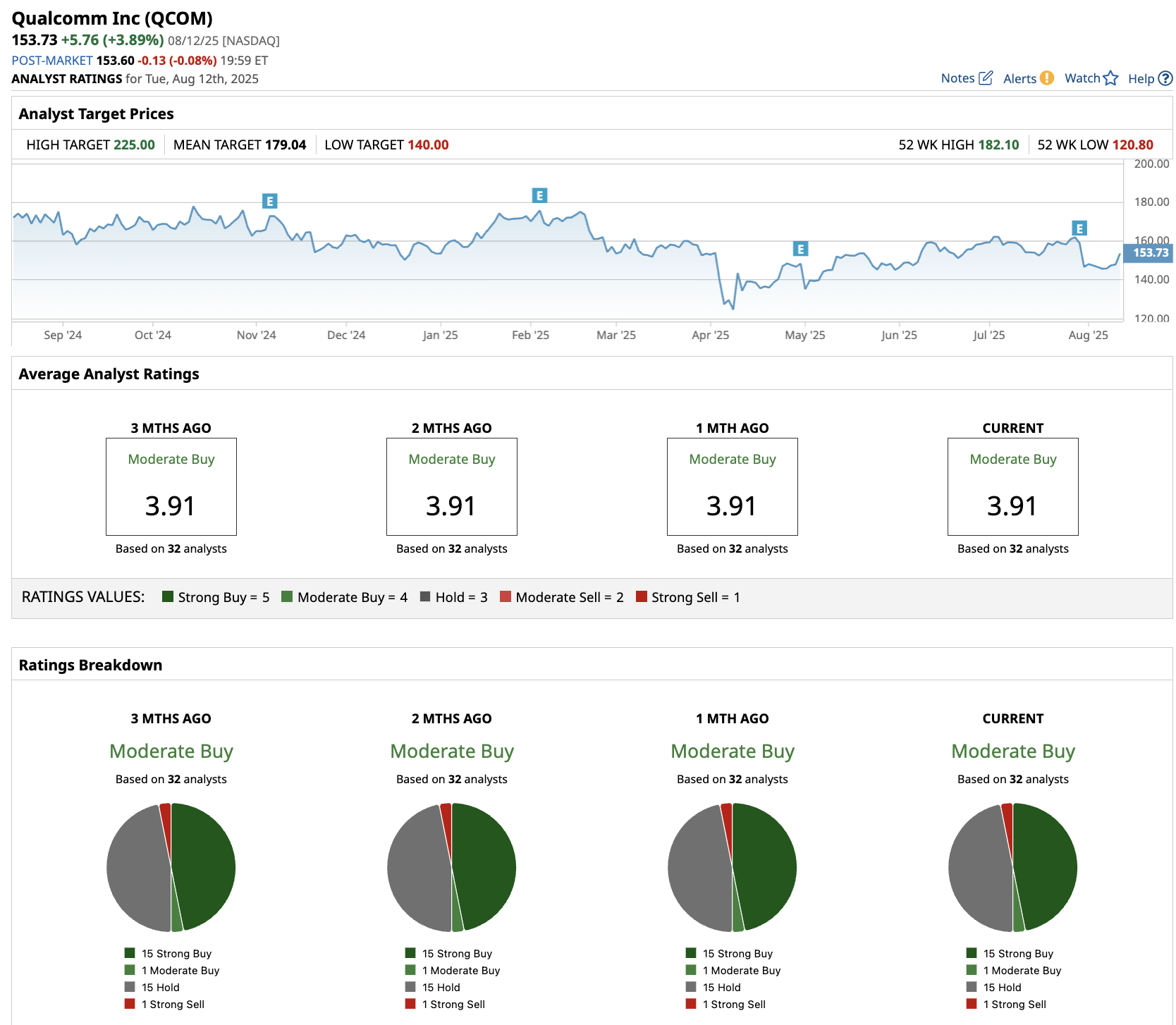

QCOM stock trades at a forward price to earnings multiple of 13x, below its 10-year historical average of 15.4x. If the chip stock is priced at 14x forward earnings, it should trade around $187 in August 2027, indicating an upside potential of 20%. If we adjust for dividend reinvestments, cumulative returns could be over 25%. Out of the 32 analysts covering Qualcomm stock, 15 recommend “Strong Buy”, one recommends “Moderate Buy”, 15 recommend “Hold”, and one recommends “Strong Sell”. The average QCOM stock price target is $179, above the current price of $154. With a fourth-quarter revenue guidance of $10.3 billion to $11.1 billion and the company trading at attractive valuations, despite its diversification progress, it is hard to see why QCOM stock dipped at all. Analysts may have a point that Qualcomm deserves more investor "respect" for its execution and growth potential beyond traditional mobile markets. On the date of publication, Aditya Raghunath did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here. |

|

|